Wifeys & Gentlemen,

As promised, welcome to part 2 of our discussion on budgeting and achieving financial goals with your significant other! I can’t think of a better way to close out June and kick off summer than a good discussion about money!

Haha, no, I’m joking! I totally can. I can think of about 1000 things I’d rather chat about the day before a holiday weekend, but this crap is important and for those of us who are trying to go on vacation or be ready to purchase a killer fall/winter wardrobe in 2017, we need this! So, bare with me, okay? I’ll try to keep this short.

Tip #6 Cold hard cash: I have heard this piece of advice for (literally) years! Stop using your damn debit and credit cards for everything you buy! Did you know that studies have shown that people tend to spend way less money when they use cash? There’s something significant (and kind of annoying) about having to see your money physically deplete from your wallet/purse that makes you 2nd guess impulsive spending. Remember the author I referenced last week? Well, Mr. Ramsey notes in his book that, in actuality, many businesses are willing to give discounts to those who use cash. Ever go to a gas station and see two different rates for cash vs credit card users? Or even better, have you ever gone to a car dealership with cash in hand instead of a charge card? You’d be amazed at the kind of deals people are willing to make to get a wad of cash from your grip. Cash is power and we should all commit to trying to use it more often. I’m going to try an experiment before the summer ends to see how much money I save when using cash vs credit. I’ll update you guys on the results!

You might even consider forgoing a formal savings account and keeping all your saved cashed in a sturdy, combination-locked safe.

Tip #7 Find a side hustle: My mother sent me a great article on Pinterest a little while ago that advised all badass ladies to find a way to make money on the side. While this might seem obvious to some, it’s not something that many of us think about. The more I read about millionaires and best practices for success, the more I see that EVERYONE (from experts to average Joes) reports that most (if not all) millionaires have multiple streams of income.

If you have the time (and even if you don’t) dedicate some of it to finding other ways to make some side cash. You could drive an Uber or Lyft a few hours a week, walk dogs, baby sit, work seasonally or on weekends at department and/or grocery stores, or even find one of those websites where you get paid to watch ads and take surveys! The possibilities are endless & anyone can do it! This extra money can be used to pay off more debt, build up your savings account, or for general needs that might come up! It’s nice to be able to contribute more money to that “overage” pot we discussed last week. Imagine, instead of $750/month left over, you have $1250! Whoa!

Caution: If you have a hard, stress filled job, please don’t start working 80+ hours a week and never have a weekend with your family or time for yourself. No amount of financial freedom is worth sacrificing your health and heart. The time for multiple income streams will come. Don’t rush it.

Tip #8 Take advantage of 401k plans (or set up a IRA when you’re ready and able): the expert author I previously mentioned would NOT agree with what I am about to say, but I did reach a certain point in his book/teachings where I started to disagree. We can get into the whys another time, but I will briefly say that for all of the advice he was giving, I began to feel like a lot of it wasn’t designed to be a “one size fits all”. While I really enjoyed his book and it is totally worth the read, I just don’t feel like all of his methods will work for everyone. No tea. No shade. 😉

I, for one, think it’s really important to have a retirement plan, even if you are still trying to pay off debt. With the direction the world is heading in, saving money for the future is just about the best/smartest thing you can do. I don’t think people in my generation (and the ones after me) can afford not to save for retirement. We all have dreams that I hope will come true, but nothing is promised to us. A failure to plan is a plan for failure and if you have a job that offers a 401k (especially if it includes matching), use it! You don’t have to contribute 10% of your paycheck. Even just 2% is a great start. Sure, it might seem illogical to be $300k in debt with a $20k retirement fund, but I don’t think (if you’re sticking to a plan that makes your income work for you) that it will cause any undo damage or harm.

Please don’t misunderstand. If you’re working a low paying job and can barely afford bus fare, don’t worry about a retirement plan right now. If you don’t work at a company that offers a plan, don’t go rushing to start an IRA until you know that you have the funds and ability to do so. I put these tips towards the end of the post because they really should be left for later; after you’ve started paying off debts, building a savings, and seeing some progress. Our finances change yearly (for the most part), so remember to be patient and give yourself time to find your groove.

Tip #9 Speaking of Investing… when you have a strong savings, money in your retirement fund, can handle all of your needs, AND have made some real progress with your debt, now is the time to start thinking about investing. I am not going to go into detail here because it can be complicated, but remember last week when we were left with about $100 in “overage” money each month? Why not use it to invest in stocks, bonds, or small businesses? There are tons of new apps and websites that allow the everyday person to make smart, diversified investments! Did you know that you can even find programs that allow customers to purchase fractional shares in smaller dollar amounts? How do you think I got in on Amazon stock?

Note: $100 a month is only $1200 per year, which doesn’t seem like much, but imagine if you know that that $1200 yearly investment has a strong chance of a 6-12% increase. Now, imagine knowing that you’re going to keep contributing every month and eventually increase those deposits from $100 to $150. Imagine knowing that 10 years from now, after you’ve moved up the ladder at work, you can contribute $300 per month to your investments.

Wifeys; Your bank account/retirement savings will be POPPIN! & that $200 worth of M.A.C makeup will feel more like $2.00. 😉

Tip #10 Wash. Rinse. Repeat: One of the newest things I’ve learned on my journey to financial freedom is that you can’t just make 1 budget and then expect for everything to stay status quo.

Honestly, you need to revisit and restructure your budget every month. Yes. Every single month.

Look: Things change all the time. We get raises and bonuses at work. We take on new jobs. We lose jobs. We have babies or adopt pets. We go back to school. We fall ill or become responsible for caring for an ill loved one. Let your commitment to yourself and your family be a weapon against that laziness I KNOW you will feel when it’s time to sit down and rewrite the budget. If not, you’re just fooling yourself into thinking you’re saving money and spending responsibly. Sure, it’s possible that for many months in the year, not much will change. However, I can almost guarantee that you’ll be surprised to discover how much extra money you didn’t know you had, just by reexamining your funds on a monthly basis. Tips 1-9 should be visited and revisited again and again. It’s smart…and good looking ;-).

Bonus tip: I know this post has gone on long enough, but I would be remiss if I didn’t mention one final thing that (I believe) is one of the most important pieces of advice I’ve received about money. Many will disagree, but I truly and firmly believe that we should all walk away and stay far away from instruments of debt!

My honest advice? When you’re ready to start building a viable financial action plan, I highly highly highly recommend making a commitment to swear off debt. No more loans, no more credit cards, no more charge accounts, and no car notes! Once these debts that you currently have are completely paid, close the accounts and walk away! I’m not going to get into a whole thing about this because it’s enough to merit a separate post on its own, but do some research. Many casual millionaires (no, not socialites or celebrities or social media influencers, but the regular people like you and me) don’t have debts outside of their mortgage payments. They drive used cars or can afford to buy a new one in cash. They don’t charge vacations or personal items to credit cards (no, not even for airline miles or cash back rewards).

Remember: Even when you’ve “arrived” at a place of financial freedom…there is ALWAYS a possibility of things going wrong. They money you have today could be gone tomorrow. Why risk being in a deficit if you don’t have to?

Sometimes, I see these Youtube celebs flexing for the internet with their new cars and ornately decorated houses and I wonder to myself…how many of these amazing people are being smart about their money? While I can’t claim to know everyone’s business, a cursory internet search might reveal more about a handful of them than meets the eye. Hey, even Kanye admitted to being in debt, and that guy has everything!

Overall, I hope this was a helpful series! Please comment and let me know if I was able to teach you something new! Are there any tips that I forgot that you believe are essential? Do you think Mrs. Renai is even more psychotic than you’d hoped?

Until Next time,

Carry on wifeys!

Love,

Mrs. Renai

🙂 ❤

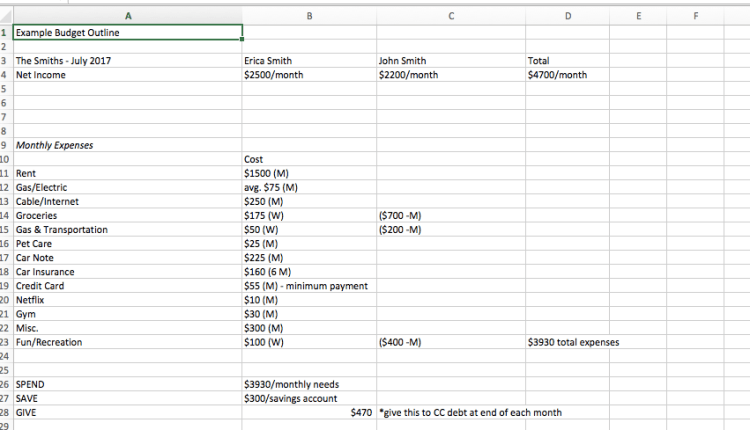

*Here is a very crude example of a budget outline. If you’re not into XCL, this is a very very very simple version that can help to get you started.